This article was originally published in Forbes.

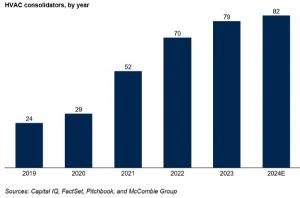

Surprisingly, the HVAC (Heating, Ventilation, and Air Conditioning) service industry has recently become a hot target for private equity (PE) investors. Five years ago, there were only a limited universe of buyers interested in these businesses. Today, the interest has exploded, with three times as many buyers vying for a piece of the action. So why are private equity firms so eager to invest in HVAC companies?

What is Private Equity?

To understand this trend, it’s essential to grasp what private equity is and how it operates. Private equity firms invest in or acquire private businesses with the goal of generating investment returns. US PE firms currently sit on nearly $1 Trillion of dry powder, or money waiting to be invested. They face pressure to deploy it effectively—if they don’t use it they risk losing it.

Most PE firms pursue a consolidation or rollup strategy. This involves using a platform company to buy and integrate smaller add-on acquisitions to quickly achieve scale. Of course, growth can be generated through opening up new cities. However, it takes significant time and investment to build brand recognition in a new area from scratch—given their short holding periods, PE generally prefers to acquire proven preexisting businesses. Upon exit, the consolidated entity captures the spread between the higher valuation multiples that larger businesses command and the lower multiples paid for the smaller purchases.

Why They Find the Industry Compelling

PE typically looks for certain fact patterns, such as highly prioritizing opportunities with stable cash flows, which provide lenders comfort. Several elements make the HVAC industry particularly attractive to these investors:

- Recession-Resistant, Essential Service: HVAC services are essential for both residential and commercial properties. Regardless of economic conditions, people prioritize getting their systems fixed above all else. This makes the industry relatively recession-resistant, providing a stable revenue stream.

- Fragmented Market with Consolidation Opportunities: The HVAC industry is highly fragmented, with many small and medium-sized businesses operating independently. Moreover, there is no clear market leader with the largest player having less than 2% market share—at best, there’s various regional champions. Whoever successfully develops a recognizable national brand is virtually guaranteed to become a billionaire.

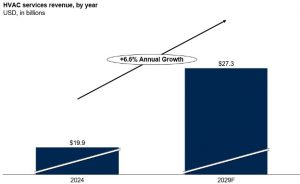

- Growth Tailwinds: The HVAC industry is expected to experience above-average growth due to several factors. Extreme temperatures cause more wear and tear on AC systems, requiring them to be replaced more often. In fact, the average lifespan of the units is 13 years, nearly ~40% lower than a decade earlier. Additionally, increasing energy efficiency standards are driving demand for retrofit installations.

Source: Mordor Intelligence

Buyer Preferences

After discussing industry trends with a half dozen HVAC consolidators, the following themes repeatedly emerged:

- Recurring Revenue: The most coveted HVAC companies generate recurring revenue through ongoing maintenance contracts. This provides a predictable income stream, which is highly attractive to lenders. Conversely, revenues associated with new construction are significantly less attractive as they are dependent upon cyclical construction (many buyers exclude businesses with more than 30% of their revenues from it).

- Loyal Labor Force: The HVAC industry is no stranger to labor shortages. Companies that have built a strong culture with below average turnover are highly marketable and command premium valuations.

- Residential vs. Commercial: Most buyers choose to exclusively focus on either residential or commercial customers. The majority prefer residential because these customers are less disciplined when it comes to getting multiple quotes for work. On the other hand, others prefer commercial as it involves a smaller number of large ongoing customers.

- Diversifying Into Complementary Services: Within their preexisting markets, many acquirers look for complementary services that can be cross-sold to their customer base. For example, commercial HVAC companies often combine with other facility maintenance categories.

Unclear How Long This Wave Will Last

As with many M&A trends, the current surge of interest in HVAC businesses will not last forever. These waves are highly influenced by market sentiment, especially if there is a high-profile failure within the industry. PE investors are herd animals; they follow trends and tend to act in unison. If there is a concern that the future pool of potential buyers will shrink, they will be reluctant to pursue new acquisitions.

Source: Capital IQ, Factset, Pitchbook

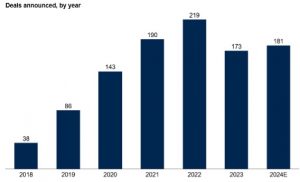

This phenomenon was evident in the 1990s when several publicly traded consolidators aggressively acquired HVAC companies. These efforts ultimately failed because the consolidators overlooked the importance of company culture and integration. As a result, the wave of interest collapsed, and it has taken nearly twenty years for similar levels of M&A interest and valuation to return. While many believe that we are in the middle innings with the number of deals peaking back in 2021, its impossible to know when the tide will recede again.

Special thanks to Norberto Gil and Michael Rodriguez in help writing this article.